|

|

IntroductionCheck out my video overview and more details below plus alternative LTC options if you want to opt-out of the LTC tax.

Michael C. Staeb, LACP, LUTCF Working with Advisors & Clients Since 2001

|

Keep reading for more info, how to opt-out, what coverage options are available, sample premiums, and a quote request form.

*** IMPORTANT UPDATE - October 9, 2021***

As of today I have no remaining LTC solutions to offer. All my carriers have suspended sales until after November 1 due to unprecedented application volumes and the short remaining timeline. I may have limited options for backdating policies but this is a gray area that comes with risks of being ineligible for an exemption. Please contact me for details.

Companies I can work with who have temporarily suspended accepting LTC application for WA residents include:

Equitable, Global Atlantic/Forethought, Guardian, John Hancock, Lincoln, MassMutual, Mutual of Omaha, National Guardian, Nationwide, OneAmerica, Securian, Pacific Life, and Transamerica.

Not a guarantee of any carrier or product availability or underwriting result.

As of today I have no remaining LTC solutions to offer. All my carriers have suspended sales until after November 1 due to unprecedented application volumes and the short remaining timeline. I may have limited options for backdating policies but this is a gray area that comes with risks of being ineligible for an exemption. Please contact me for details.

Companies I can work with who have temporarily suspended accepting LTC application for WA residents include:

Equitable, Global Atlantic/Forethought, Guardian, John Hancock, Lincoln, MassMutual, Mutual of Omaha, National Guardian, Nationwide, OneAmerica, Securian, Pacific Life, and Transamerica.

Not a guarantee of any carrier or product availability or underwriting result.

What It *Is*Funded through a new payroll deduction tax on W-2 employees in WA State, this legislation is a first in the country attempt at creating basic long-term care benefits for state residents.

|

What It *Isn't*While well intentioned, the implementation of this legislation has a number of concerning 'holes' that as of early May 2021 have no resolution for residents.

|

Outside References and Articles

* Genworth Financial's 2020 Cost of Care Survey

** AALTCI.org - 2014 Genworth study - average length of claim if more than 1 year

** AALTCI.org - 2014 Genworth study - average length of claim if more than 1 year

How To Opt-OutThe legislation includes a provision to qualify for an exemption from the LTC tax by having your own "long-term care insurance" inforce no later than November 1, 2021. According to Nationwide's review of the law, the following coverage types should qualify for an exemption:

⦿ Long-term care riders on life insurance and annuities ⦿ Qualified long-term care insurance contracts ⦿ Long-term care riders or policies purchased under group coverage |

OPT-OUT DEADLINE

NOV 1, 2021 |

|

Opt-Out Process

The exemption filing period opens up on October 1, 2021 and closes December 31, 2022. As of early May 2021 what is known of the opt-out process is that it will consist of each WA resident logging into the Employment Security Department (ESD) website and completing an application for the exemption. It is not yet known what documentation of private insurance will be required, but a declaration page or summary benefit statement showing a coverage effective date prior to November 1, 2021 would be a reasonable assumption. Once approved for an exemption each resident will receive a letter from ESD documenting they are exempt from the tax. You should keep this letter and provide a copy to any employer who pays you W-2 compensation. Without the letter the employer is required to collect the tax from your pay. |

Ready to Opt-Out?

Talk to your insurance professional or contact us. If your existing professional would like assistance in implementing an opt-out solution for you we can help them do that!

Request a quote or reach out if you have questions.

>>> READ IMPORTANT UPDATE ABOVE BEFORE REQUESTING A QUOTE <<<

Request a quote or reach out if you have questions.

>>> READ IMPORTANT UPDATE ABOVE BEFORE REQUESTING A QUOTE <<<

Or keep reading for opt-out options... |

|

Private LTCi Solutions

Below are a few key pros and cons of each of the three types of insurance-based long-term care solutions.

Traditional LTCiPROS:

CONS:

|

Hybrid LTCiPROS:

CONS:

|

LTC RidersPROS:

CONS:

|

† These are all carriers in these product categories that Michael Staeb can worth with. He may recommend only 2-3 best suited to your individual circumstances. Washington State will not certify that any specific product will make you eligible for an exemption from the tax, only referring to "long-term care insurance" as defined in RCW 48.83.020. Michael Staeb nor any insurance company or agent can guarantee that any specific product will or will not qualify under Washington Long-Term Care Trust Act or any subsequent amendments or regulations.

Don't Wait - Get Started Now!

The November 1, 2021 deadline is when you must have coverage inforce by, not simply applied for. Please do not wait until the last minute to apply for private coverage. If we cannot get you through underwriting in time for the deadline you will be stuck paying the tax under the current version of the law (as of early May 2021). I recommend applying no later than September 1, 2021. This reduces your chances of not having coverage in place by the November 1 deadline. There will be a rush of late applicants and inevitably some will not get coverage in time. Here's what you might experience for turnaround times:

|

Accelerated Underwriting

Generally available to clients with clear medical history and a healthy profile (build, no tobacco, minimal prescriptions, etc.)

e-Application and e-Signature ‡ Personal history interview (phone or online) No exam. No Labs. No Medical Records. 3-5 days or up to 2 weeks (you can apply as accelerated and if you are disqualified you simply switch to a regular underwriting process) |

Regular Underwriting

Generally available to clients with clear medical history and a healthy profile (build, no tobacco, minimal prescriptions, etc.)

e-Application and e-Signature ‡ Exam and labs based on age and amount applied for Medical records at underwriter discretion 3-6 weeks (possibly longer based on how quickly your health care provider(s) supply your medical records) |

These are estimated turnaround/processing times only. They are not a guarantee that you can get coverage within these time frames.

‡ Process will vary some from one insurance company to the next. e-Application not available for traditional long-term care insurance.

‡ Process will vary some from one insurance company to the next. e-Application not available for traditional long-term care insurance.

Sample Pricing

These are examples only and not a guarantee of any coverage availability, underwriting class, or benefits.

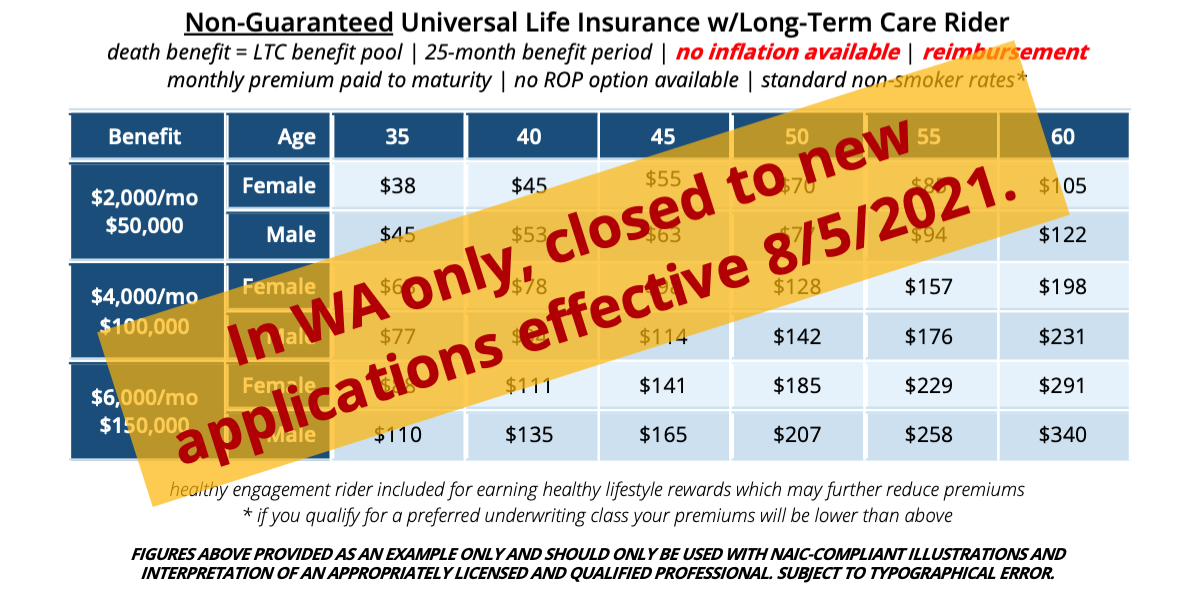

LTC Riders (basic non-guaranteed plan)

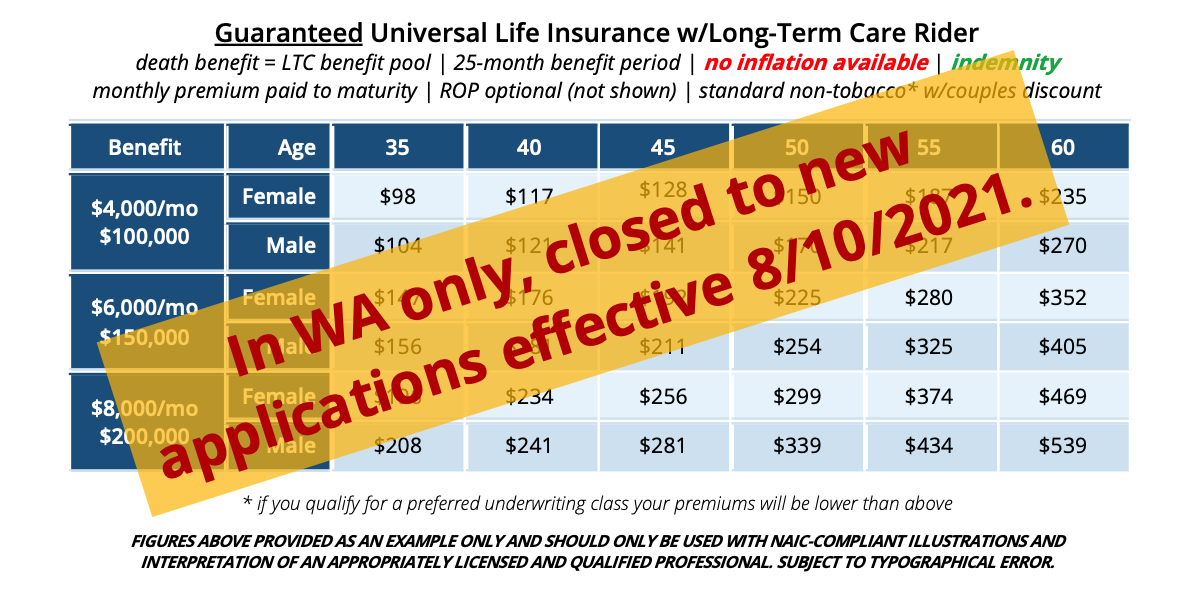

LTC Riders (basic guaranteed plan)

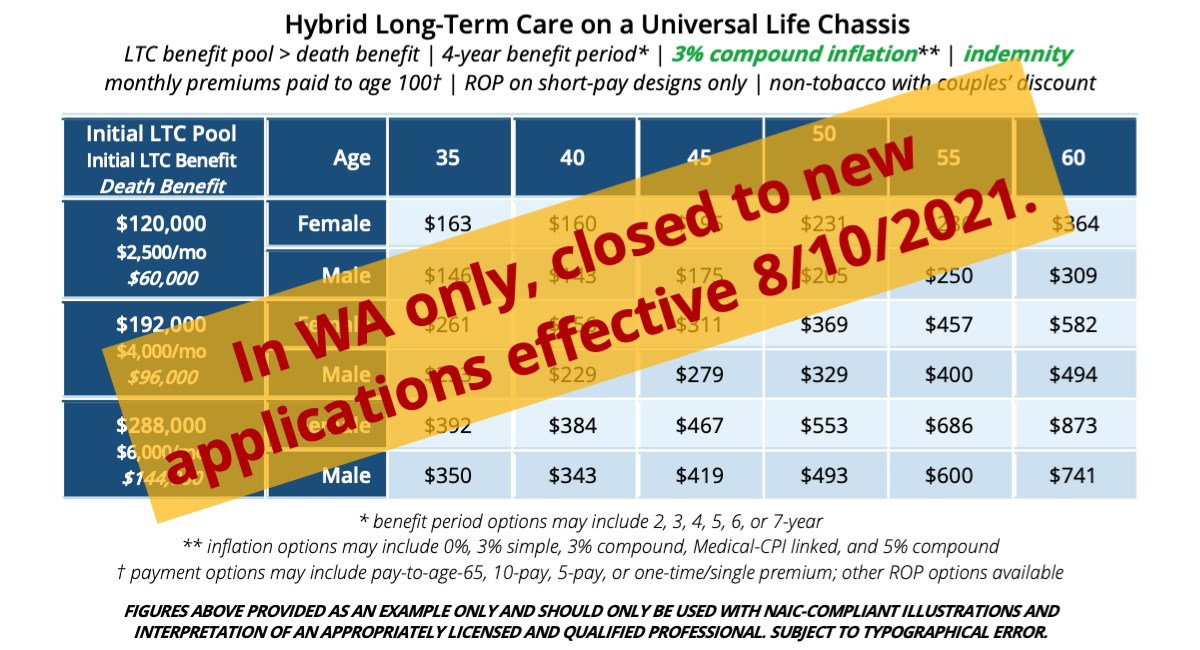

Hybrid LTCi (more comprehensive guaranteed plan)

Ready to Opt-Out?

Talk to your insurance professional or contact us. If your existing professional would like assistance in implementing an opt-out solution for you we can help them do that!

Request a quote or reach out if you have questions.

>>> READ IMPORTANT UPDATE ABOVE BEFORE REQUESTING A QUOTE <<<

Request a quote or reach out if you have questions.

>>> READ IMPORTANT UPDATE ABOVE BEFORE REQUESTING A QUOTE <<<